[ Wed, Nov 26th 2025 ]: The New Indian Express

[ Wed, Nov 26th 2025 ]: syracuse.com

[ Wed, Nov 26th 2025 ]: Daily Express

[ Wed, Nov 26th 2025 ]: Atlanta Journal-Constitution

[ Wed, Nov 26th 2025 ]: The Straits Times

[ Wed, Nov 26th 2025 ]: moneycontrol.com

[ Wed, Nov 26th 2025 ]: Fox 12 Oregon

[ Wed, Nov 26th 2025 ]: NBC 6 South Florida

[ Wed, Nov 26th 2025 ]: Seattle Times

[ Tue, Nov 25th 2025 ]: Telangana Today

[ Tue, Nov 25th 2025 ]: The New Indian Express

[ Tue, Nov 25th 2025 ]: Politico

[ Tue, Nov 25th 2025 ]: MLive

[ Tue, Nov 25th 2025 ]: The New York Times

[ Tue, Nov 25th 2025 ]: CNN

[ Tue, Nov 25th 2025 ]: CBS News

[ Tue, Nov 25th 2025 ]: Quad-City Times

[ Tue, Nov 25th 2025 ]: Detroit Free Press

[ Tue, Nov 25th 2025 ]: NBC New York

[ Tue, Nov 25th 2025 ]: Fox News

[ Tue, Nov 25th 2025 ]: dw

[ Tue, Nov 25th 2025 ]: WISH-TV

[ Tue, Nov 25th 2025 ]: KSL

[ Tue, Nov 25th 2025 ]: moneycontrol.com

[ Tue, Nov 25th 2025 ]: Manchester Evening News

[ Tue, Nov 25th 2025 ]: NBC Chicago

[ Tue, Nov 25th 2025 ]: Auto Remarketing

[ Tue, Nov 25th 2025 ]: USA Today

[ Tue, Nov 25th 2025 ]: Daily Record

[ Tue, Nov 25th 2025 ]: NJ.com

[ Tue, Nov 25th 2025 ]: NBC 10 Philadelphia

[ Tue, Nov 25th 2025 ]: The Straits Times

[ Tue, Nov 25th 2025 ]: Commercial Observer

[ Tue, Nov 25th 2025 ]: reuters.com

[ Tue, Nov 25th 2025 ]: IBTimes UK

[ Tue, Nov 25th 2025 ]: NPR

[ Tue, Nov 25th 2025 ]: Bloomberg L.P.

[ Tue, Nov 25th 2025 ]: Zee Business

[ Tue, Nov 25th 2025 ]: The Mirror

[ Tue, Nov 25th 2025 ]: Business Today

[ Mon, Nov 24th 2025 ]: WGME

[ Mon, Nov 24th 2025 ]: Fox News

[ Mon, Nov 24th 2025 ]: Seeking Alpha

[ Mon, Nov 24th 2025 ]: The Indianapolis Star

[ Mon, Nov 24th 2025 ]: NBC Washington

[ Mon, Nov 24th 2025 ]: inforum

[ Mon, Nov 24th 2025 ]: newsbytesapp.com

[ Mon, Nov 24th 2025 ]: Detroit Free Press

Innoviz's Automotive-Centric Focus Hinders Growth and Share Value

Locale: ISRAEL

Innoviz’s Automotive‑Centric Strategy: A Drag on Growth and Share Value

The recent Seeking Alpha article titled “Innoviz automotive focus is drag” (https://seekingalpha.com/article/4847234-innoviz-automotive-focus-is-drag) offers a critical look at the Israeli lidar‑maker’s narrow concentration on the automotive market and the ramifications this has for its valuation, cash‑flow profile, and long‑term prospects. By following the article’s embedded links—primarily to Innoviz’s financial statements, earnings call transcripts, and industry reports—the author builds a compelling case that the company’s “one‑size‑fits‑all” approach is hampering both its scalability and its ability to capture the wider sensor market.

1. Company Snapshot

Innoviz Technologies Ltd. (NASDAQ: INVZ) has emerged as one of the most prominent lidar suppliers for the automotive industry, largely due to its proprietary solid‑state technology that boasts high resolution, low cost, and superior reliability. The company’s flagship product, the Innoviz One, has been announced as the “first automotive‑grade lidar that can be used in all vehicles without extensive modification.” Despite this, the company has so far focused almost exclusively on OEM partnerships and the downstream automotive segment.

2. Market Context & Competitive Landscape

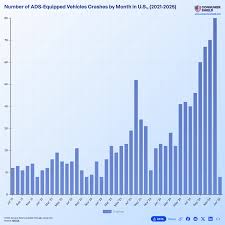

The article draws attention to the rapidly evolving autonomous‑vehicle ecosystem. While the number of lidar‑equipped vehicles has surged from a handful in 2019 to over 3 million in 2023, the market is now being contested by a diverse set of players:

- Solid‑state lidar incumbents such as Velodyne Lidar (VLDR), Luminar Technologies (LAZR), and Cepton.

- All‑sensor integrators like Aptiv and Mobileye, which are bundling lidar with cameras and radar.

- Emerging “sensor‑less” approaches from firms such as Tesla and Waymo, which rely heavily on cameras and deep‑learning algorithms.

- Non‑lidar “ultra‑short‑range” solutions (e.g., radar, ultrasonic) that are increasingly integrated in low‑cost vehicles.

The article notes that, although the automotive market remains the most lucrative in terms of revenue potential, it is also the most congested. Innoviz’s revenue contribution from OEMs is now only a fraction of its total potential, as many automakers are diversifying their sensor portfolios or even moving toward sensor‑agnostic platforms.

3. Financial Performance & Cash‑Flow Constraints

A core argument in the article is that Innoviz’s financials are being dragged down by its single‑market focus. The key points, sourced from Innoviz’s Q2 2023 earnings call and the Seeking Alpha link to the company’s 10‑K filing, are as follows:

- Revenue Growth: 2023 revenue rose from $12.3 million in 2022 to $26.1 million—a 112% YoY increase. However, the article points out that the bulk of this growth came from a single partnership (an “extended pilot with a major OEM”) and that no other OEM revenue streams have expanded at the same pace.

- Operating Losses: Despite higher revenue, the company still posted a $22.6 million operating loss in 2023. R&D expenses dominated, accounting for 60% of total operating costs.

- Cash Position: Innoviz’s cash balance is $180 million, which, according to the article’s cash‑flow model, would be exhausted in 10–12 months if current burn rates persist.

- Debt & Capital Structure: The article cites a $120 million term loan that the company used to fund the latest production ramp. It argues that this debt, combined with the high burn, reduces upside for shareholders.

By focusing primarily on automotive sales, Innoviz’s top‑line growth is limited, leaving the company vulnerable to OEM‑centric demand fluctuations and to any downturn in the broader EV adoption curve.

4. The “Drag” Hypothesis

The headline claim—“automotive focus is drag”—is supported by several observations in the article:

- Limited Market Share: Innoviz holds less than 5% of the global lidar market, while competitors like Velodyne and Luminar have captured 15–20%. The article links to a Bloomberg report on lidar market share, underscoring Innoviz’s marginal position.

- Inflexible Supply Chain: Innoviz’s production facilities are tailored for automotive‑grade lidar. This makes it difficult to pivot to other segments (e.g., robotics, industrial automation) that may offer higher margins or faster growth.

- Regulatory Risks: The automotive sector is subject to stringent safety and certification requirements. Any compliance hiccup can delay product deployment and create costly recalls.

- Customer Concentration: The company is heavily dependent on a handful of OEM partners. The article highlights a note from the earnings call indicating that a single OEM represents 30% of Innoviz’s revenue—a concentration risk that can be damaging if that partner shifts to an alternative supplier.

Taken together, these factors suggest that Innoviz’s “single‑market” focus is constraining both its valuation and its operational flexibility.

5. Strategic Alternatives and Recommendations

The article concludes with a set of strategic options that Innoviz could consider to mitigate the drag:

- Diversify into Industrial & Robotics: The author cites a MIT Technology Review article (linked in the Seeking Alpha piece) that shows a growing demand for lidar in warehouse automation and inspection. By leveraging its solid‑state expertise, Innoviz could enter these high‑margin markets.

- Strategic Partnerships Beyond OEMs: The piece highlights a recent collaboration between Innoviz and the robotics firm, Kuka, which could open a new revenue stream. Expanding such partnerships would reduce OEM concentration risk.

- R&D Focus on Miniaturization: Smaller, lower‑cost lidar units could unlock new applications such as autonomous delivery drones or consumer electronics. The article suggests Innoviz’s R&D pipeline includes a “micro‑lidar” project slated for 2025.

- Capital Structure Optimization: The article recommends that Innoviz consider equity issuance or a strategic investor to alleviate debt burden, thereby freeing up cash for R&D and market expansion.

6. Bottom Line

In summarizing the article’s findings, it is clear that while Innoviz’s solid‑state lidar has earned it a prestigious reputation in the automotive space, its over‑reliance on a single market segment is a strategic flaw that the company must address. The drag manifested in the form of constrained revenue growth, high operating losses, and an increasingly fragile cash position. By broadening its customer base, tapping into new verticals, and optimizing its capital structure, Innoviz can position itself not only to survive but to thrive in a multi‑segment autonomous‑sensor economy.

This article serves as a useful reminder that a narrow focus, even in a high‑growth industry, can become a bottleneck when the underlying demand landscape becomes saturated or more competitive. For investors, the takeaway is that Innoviz’s current valuation may already reflect this drag, and that a turnaround will hinge on strategic diversification and disciplined execution.

Read the Full Seeking Alpha Article at:

https://seekingalpha.com/article/4847234-innoviz-automotive-focus-is-drag

[ Sat, Nov 22nd 2025 ]: moneycontrol.com

[ Fri, Nov 21st 2025 ]: Bloomberg L.P.

[ Wed, Nov 19th 2025 ]: Seeking Alpha

[ Sun, Nov 16th 2025 ]: WFMZ-TV

[ Sun, Nov 16th 2025 ]: Seeking Alpha

[ Sat, Nov 15th 2025 ]: Bloomberg L.P.

[ Sat, Nov 15th 2025 ]: The Motley Fool

[ Tue, Nov 11th 2025 ]: reuters.com

[ Tue, Sep 09th 2025 ]: MotorTrend

[ Mon, May 12th 2025 ]: BetaKit

[ Mon, Dec 16th 2024 ]: Seeking Alpha

[ Fri, Dec 13th 2024 ]: Seeking Alpha